Reformulating energy portfolio strategies for the transition towards the low carbon emission futures

Cau Thai | 4th March 2021Dr. Cau Thai, Principal Consultant of Oakley Greenwood shares his thoughts on why an energy market participant no matter how small or large needs to critically review and to reformulate their strategies to respond to changes in the energy industry as it transitions towards a decarbonised future. He also lists some initial questions to facilitate that strategy reformulation.

The change drivers

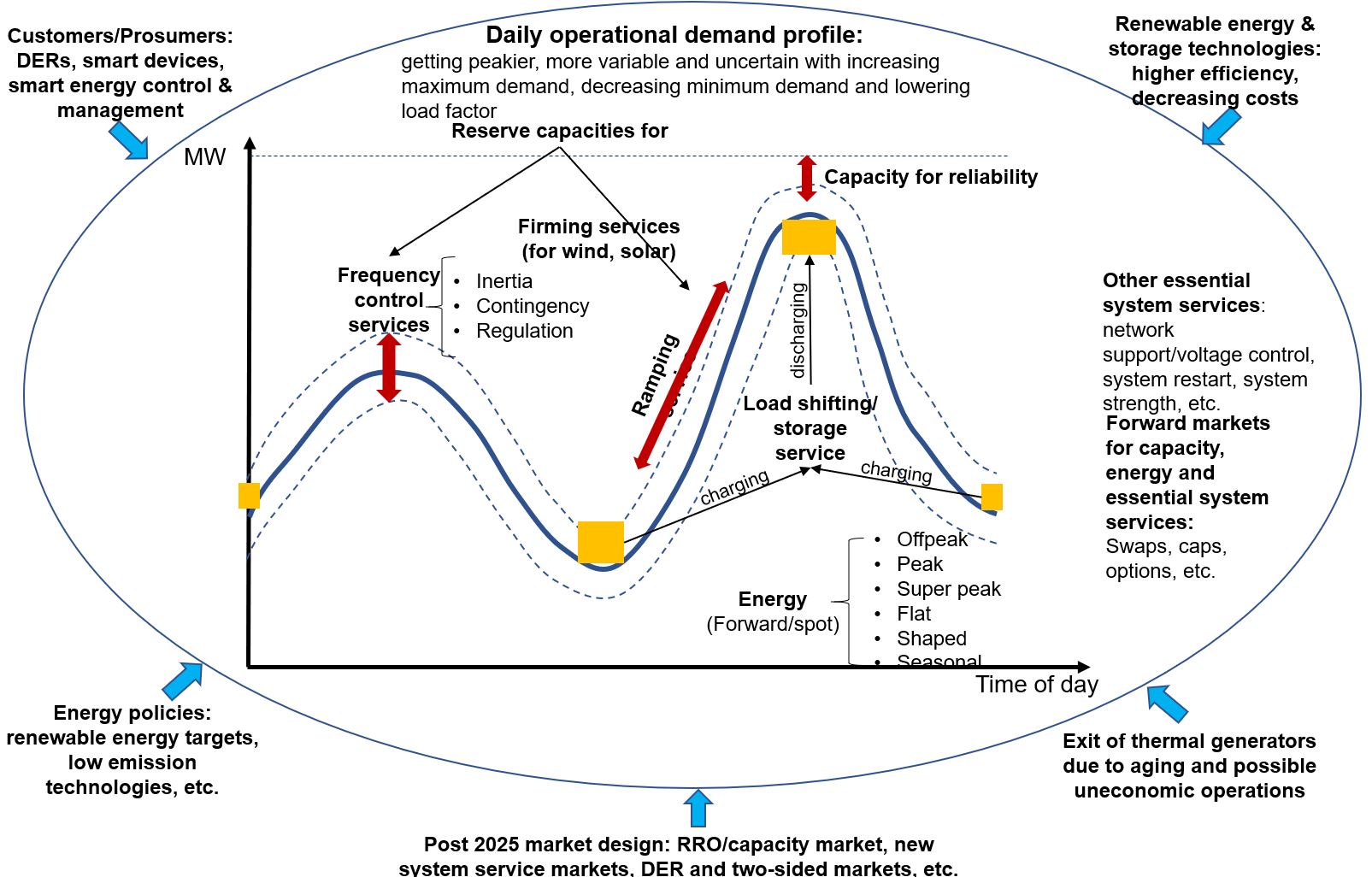

Perhaps everyone with interest is already very familiar about the ongoing changes in the energy industry as it transitions towards a low carbon emission future. These changes and their impacts are illustrated in the simple diagram below.

The key change drivers include renewable energy and storage technologies, new customer needs, decarbonised energy policies, exit of thermal generators and the post 2025 market design. The renewable energy targets of both federal and state governments together with the decreasing cost of renewable energy and energy storage technologies have driven increasing penetration of renewable energy into the NEM. The supply side also faces the gradual exit of existing large thermal generation reaching their technical lifetime and possibly early exit due to the likely uneconomic operation when competing against the zero marginal production cost of the “subsidised” renewable energy. On the demand side, there have been increasing installations of rooftop PV, smart meters, energy efficient equipment, smart energy control devices and battery storage systems. These distributed energy resources (DER) have enabled customers to become more responsive to market prices and hence more participative in consuming and generating into the energy markets.

Impacts

These changes impose challenges to the power systems and create new market needs in a number of ways:

- Power systems security: The increasing variabilities and uncertainties of both supply and demand have created challenges to short-term and instantaneous supply and demand balance of power systems and increased the risks of blackouts. As a result, this has increased the cost of providing essential system services (previously called ancillary services) and has required consideration of separate services such as inertia, very fast frequency services, operating reserve (for ramping), system strength, etc. Previously these services have been available as aggregated by-products from existing ancillary services or through directions or interventions by system operators;

- Power system reliability: The future exit of synchronous and dispatchable thermal generation and the non-firm output of renewable energy have created concerns about the long-term supply adequacy of power systems. The current energy-only market design like that of the NEM may not be effective enough to provide early signals for timely capacity investment for supply adequacy;

- New wholesale needs: Variable and non-controllable renewable energy needs to work in tandem with controllable capability from traditional and new sources including capacity firming services, energy load shifting and dispatchable and flexible generation. The central scenario of the AEMO’s 2020 Integrated System Planning (ISP) shows that the majority of new dispatchable capacity over 2021-2042 will be energy storage with more than 15 GW of new capacity of different storage durations; and

- New end-use customers’ needs: The active customers (prosumers/gensumers or more engaged customers) will require innovative retail energy products and new market mechanisms to reward the growing flexibility of their demand responses.

To address these challenges and to meet the arising needs from the changes, the Energy Security Board’s post 2025 market design project has considered a number of potential redesign options such as a modified Retailer Reliability Obligation (RRO) or a capacity market, new markets or mechanisms for some essential system services of priority, mechanisms for DER integration and two-sided markets. This project is a significant change driver to the energy markets in itself as it will significantly influence the way market participants make capacity investment decisions now and will commercially operate in the energy and related markets in future.

So, in which directions would the changes impact on the energy industry and are they predictable? The simple answer is depending on how major drivers are going to unfold, the energy market can end up moving in different directions. We qualitatively discuss just few possible directions as below:

- Different energy futures: There is no single predictable future scenario of the NEM in the next 20 years. The future paths are subject to how the forthcoming energy policies unfold, how quickly the technologies advance and how quickly customers adopt new technologies. To reflect that, the AEMO’s 2020 ISP has defined 5 different future states (futures/scenarios) based on different levels of DER uptake, energy demand and renewable energy penetration;

- Variable and uncertain operational demand profile: It is expected that with the increasing penetration of rooftop PV and other non-scheduled renewable energy, the operational demand, which is the net of native demand of customers and those resources, will be increasingly variable and uncertain. This net demand profile will get peakier with lowering load factor. The variability and uncertainty will be further exacerbated by the intermittent supply of a growing amount of large-scale grid-connected renewable energy (wind and solar farms). But this might be smoothed out over time with the increasing investment in energy storage both at grid-scale and end-use customer levels. Timing will be everything: will there be an initial increase in volatility eventually dampened by storage or will storage dominate immediate investment and the possible volatility ‘fizz? Will the changes depend on location across the NEM given different availability of intermittent resources and also incumbent thermal plants as they might to some extent complement each other?

- Unclear strategic behaviours of market participants: The strategies of participants across long or medium-term horizons will be critical. Some major participants have already taken positions or made announcements about investment in large energy storage capacity. While the economic efficiency of these investments from the system perspective remains to be seen, they can certainly change the competition landscape to which other participants might have to adapt. Given uncertainties, smaller participants might adopt wait-and-see strategies as they can contract in the medium term. The theoretical studies and past practical experience suggest that over investment would result in low contract levels and low spot prices, and that given sufficient capacity, over contracting would lead to lower spot prices and vice versa. In the future while some of these principles might hold, the interactions between investment, forward contract and spot markets with abundant renewable energy and energy storage need to be reviewed and further studied; and

- Volatile spot market prices: Given the variable and uncertain demand and unclear medium-term contracting strategy, it can be expected that the spot price will become increasingly more volatile. This might be the case until sufficient energy storage capacity enters the market and when some short-term forward market (say a day ahead type) is introduced. The spot price volatility might be reduced because storage reduces variability and uncertainties of the operational demand and short-term forward market reduces the spot exposure (the uncontracted part) of the physical assets that generators would exercise market power if there is any opportunity.

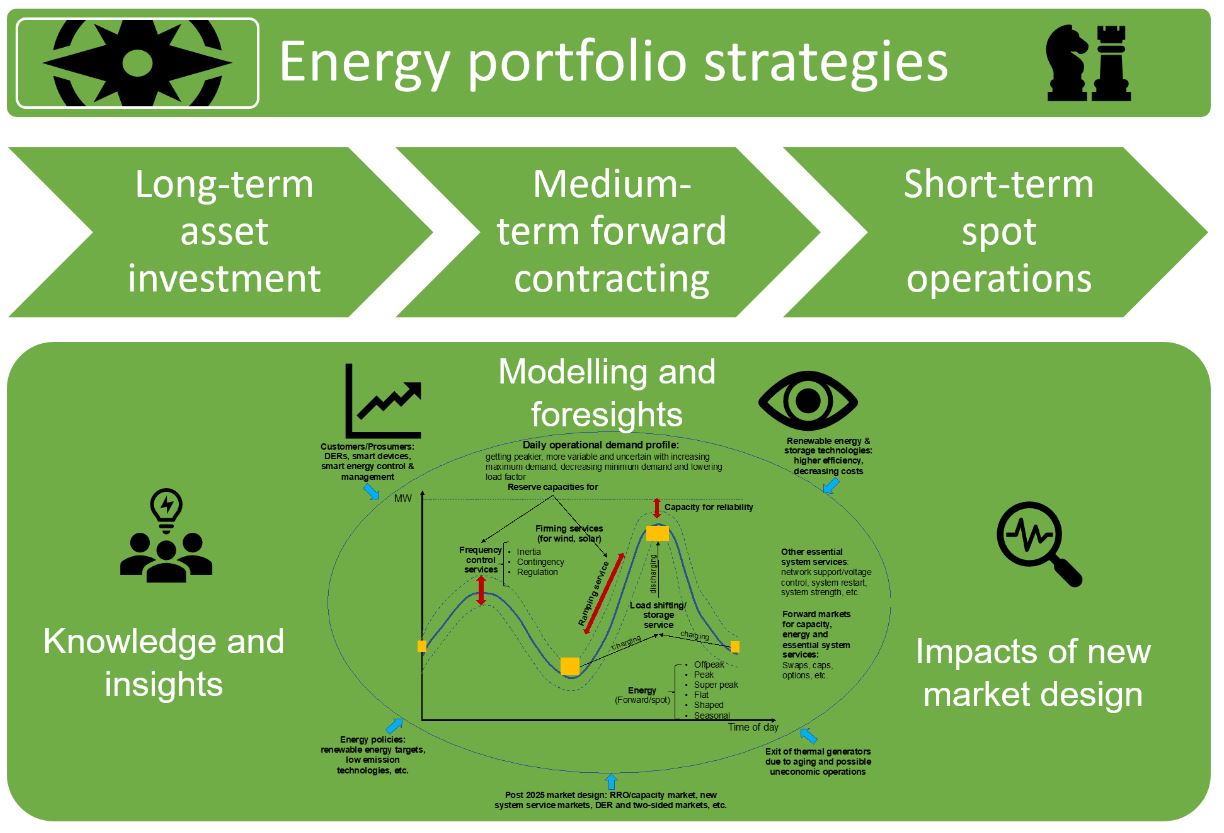

While the energy industry faces a lot of uncertainties and can trend towards any of the different futures, it is clear that existing energy portfolio strategies need to be critically reviewed and reformulated. During this process, some strategic questions can be raised under the strategic themes shown in the following diagram and summarised after that.

Reformulating energy portfolio strategies

- Knowledge and insights: Do we actually have sufficient knowledge and insights about the changes? How do we know that we know? What do emergent needs such as system strength, inertia, fast frequency response and operating reserves (for increasing ramping needs) mean? What technologies could supply these? While the changes above are deep rooted in how power systems are operated within their associated constraints (frequency, voltage, etc), relevant inter-disciplinary parts of economics, operations research (optimisation), commerce and business strategy are also required to develop insights.

- Impact of newly designed markets or mechanism: What are the directions of the new post 2025 market design elements? How will the revised RRO or capacity market, system services markets, two-way markets impact capacity investment, the current markets (wholesale, retail, forward, spot) and the products and services we could provide?

- Modelling and foresights: Based on the above understanding, how would our competitors and customers respond to changes? Do current strategies and announcements of capacity investment make sense? How would those responses impact our strategies and revenue/profitability? Would the existing market models be able to incorporate the new changes? Do we need new market modelling? How can we be confident to use existing or new models to provide foresights and to inform our business strategies and decisions?

- Energy portfolio strategy review: How would all of the changes above impact our current strategies on asset investment, hedging products and contracting, and spot trading? What is our positioning strategy? Should we lead the changes or be led by them? Should we invest or hedge (contract)? How would we allocate the resource (capacity, energy) to different products (capacity, energy, ancillary services) and markets (forward, spot) to maximise asset values? Do current strategies need to be reformulated? Given the new and more stringent intertemporal constraints such as storage duration, ramp rate capabilities and highly uncertain environments (policies, technologies, market design), existing energy portfolio strategies should be holistically and carefully reviewed and reformulated.

- Long-term asset investment strategy: What services can our new assets provide? What are the values from those services? Who are the existing or potential buyers (AEMO, TNSPs, DNSPs, generators, retailers, end-use customers, or traders)? What risks do we have from the uncertain change drivers such as energy policies, market design and technologies? Past experience indicated that a mistake in long-term investment decision could cost dearly.

- Medium-term hedging strategies: Given existing and new assets and the potentially more volatile and uncertain markets, how would we hedge the value of assets? What would be the new financial contracts (capacity firming, load shifting/ storage products, super peak, new off-peak products) that we should trade? Would we create or customise ones to suit our asset generation and/or customer load profiles? Are there any products that if added would enhance the values of our existing portfolio of assets and contracts, for example, increase the firmness of capacity of the whole portfolio? Often these financial products can serve different roles. For example, a capacity product can serve as capacity for reliability, for frequency control reserves and for firming renewable output. How can we price them properly?

- Short-term trading strategies: Given our portfolio of physical assets and financial hedging contracts have been set ahead, how would we defend those contract positions and maximise the value of the net position (balance between actual physical assets, customer consumption profiles and contracted positions) in the spot energy market and essential system services markets? The spot trading strategies would become more complex in a likely more variable and uncertain environment of short-term markets.

These questions are by no means exhaustive. Each energy market participant has their own existing generation asset base, customer base, market positioning and return-risk preferences. Each thus has their own set of specific and related questions and problem statements. We however believe they would serve as starting points to provoke some deeper thoughts and other specific questions regarding strategic responses to changes.

Oakley Greenwood

OGW team of experts have extensive experience in power systems operation and planning, market design and regulation, and energy portfolio strategies (asset investment, hedging products, contract and spot trading strategies). We are able to assist energy market participants, investors, new entrants and stakeholder organisations to address those questions and other specific questions. Please contact Greg Thorpe (gthorpe@oakleygreenwood.com.au) or Dr. Cau Thai (cthai@oakleygreenwood.com.au) should you have any related inquiries.